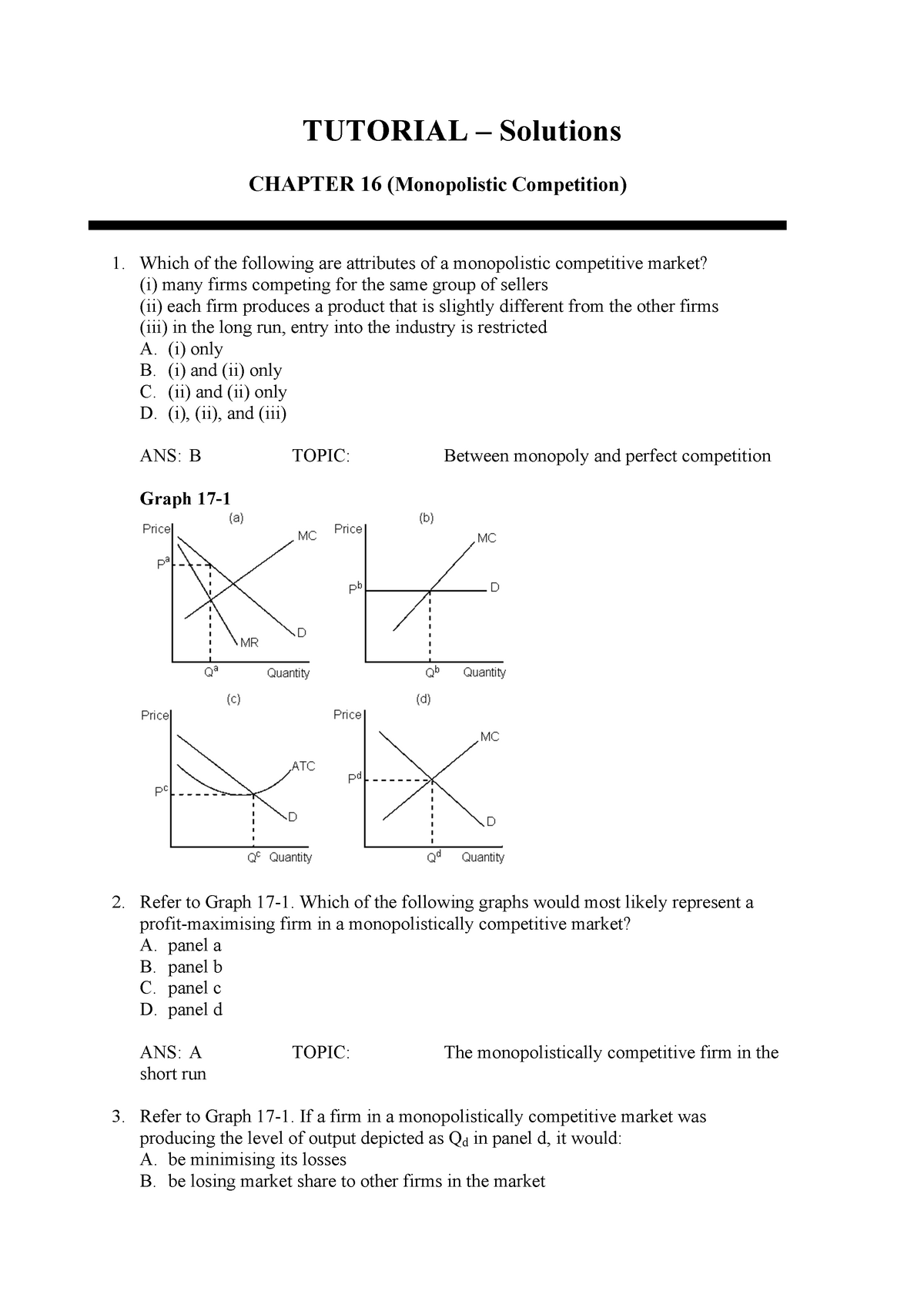

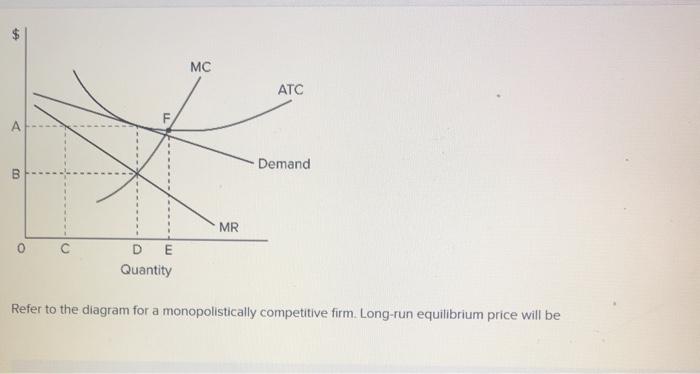

41 refer to the diagram for a monopolistically competitive firm. long-run equilibrium price will be

a) Describe the factors that drive profits to zero in perfectly competitive markets in the long run. Explain carefully the incentives that drive the market to a long run equilibrium. The biggest factor driving this is the free entry/exit of firms in the long run, and that firms are selling identical products.

A. Both purely competitive and monopolistic firms are "price takers." B. Both purely competitive and monopolistic firms are "price makers." C. A purely competitive firm is a "price taker," while a monopolist is a "price maker." D. A purely competitive firm is a "price maker," while a monopolist is a "price taker."

The graph shows that: - ScieMce. Refer to the graph shown of a monopolistically competitive firm. The graph shows that: asked Sep 2, 2019 in Economics by livdinome. A. new firms will enter the industry. B. some existing firms will leave the industry. C. the price of the product is $90. D. the industry is in long-run equilibrium.

Refer to the diagram for a monopolistically competitive firm. long-run equilibrium price will be

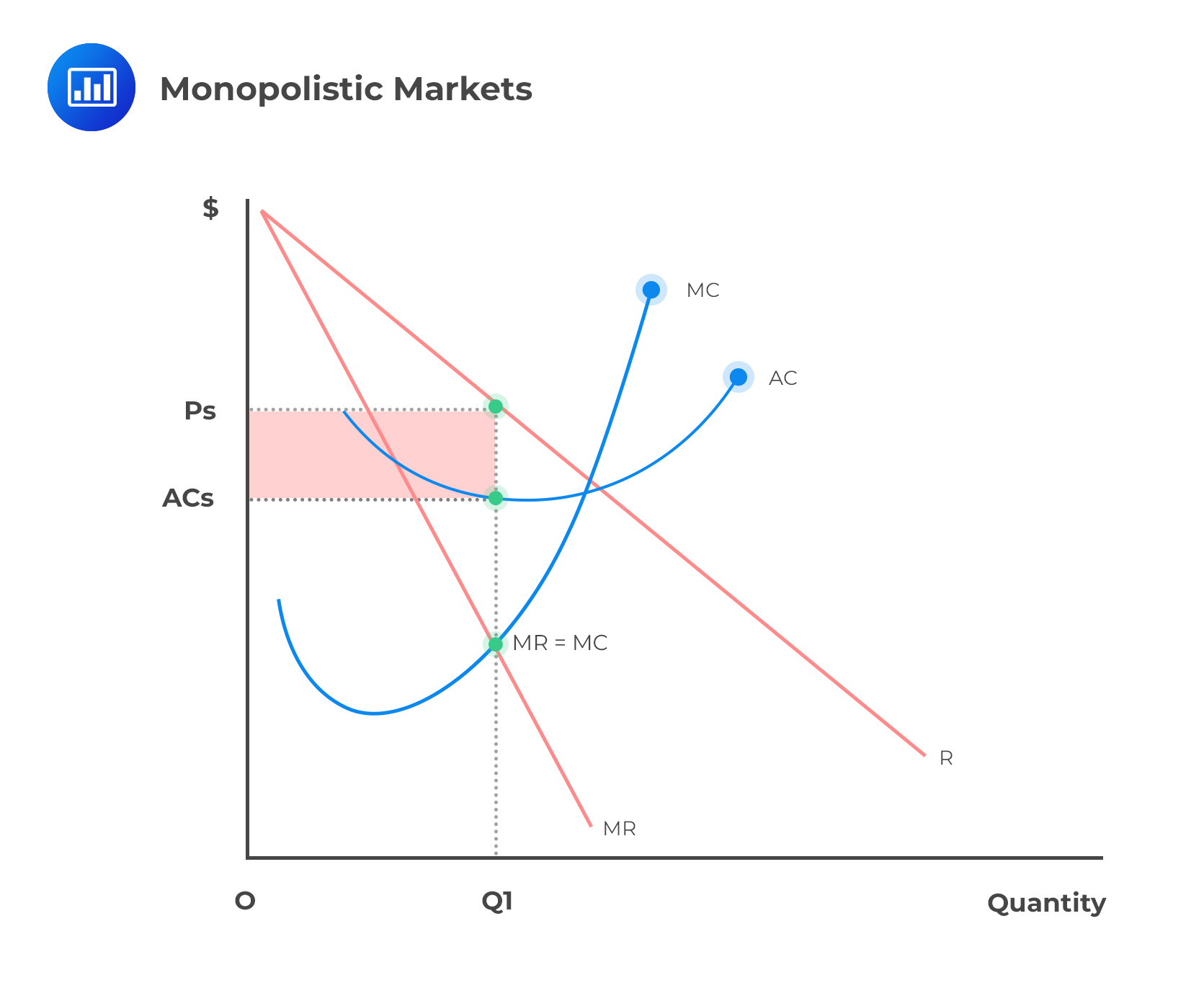

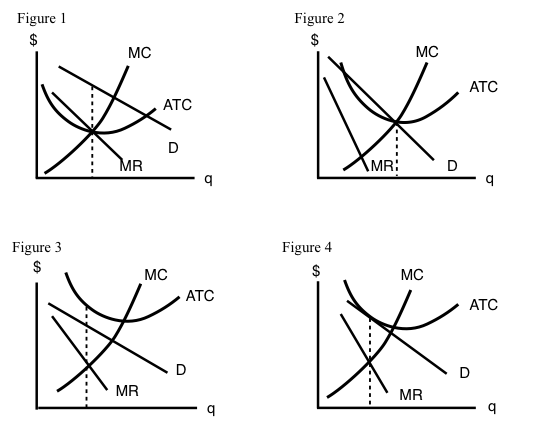

The diagram below shows demand and cost curves for a monopolistically competitive firm. FIGURE 11-3 19) Refer to Figure 11-3. A monopolistically competitive firm is allocatively inefficient because in the long-run equilibrium A) MC is greater than price. B) price is greater than LRAC at QL.

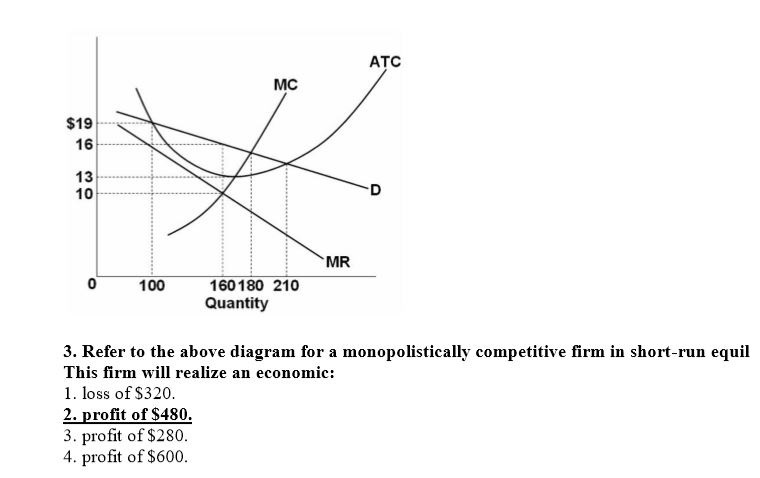

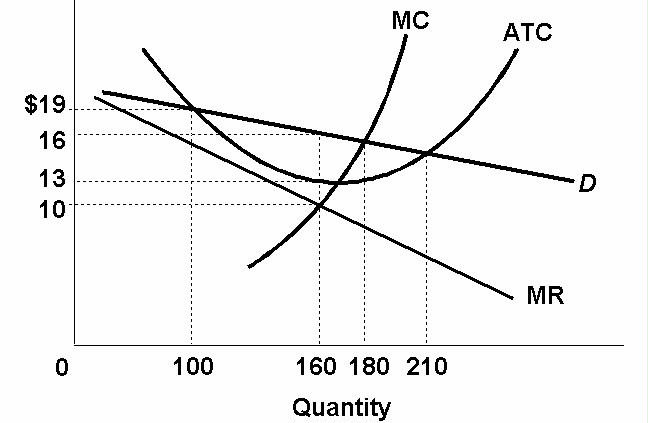

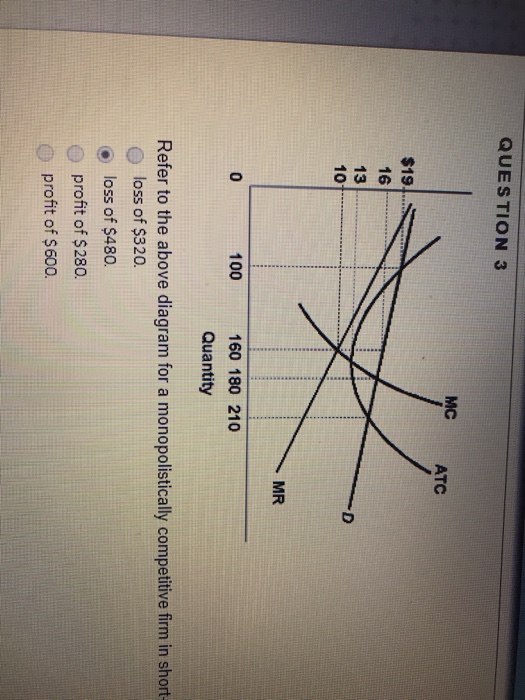

Refer to the diagram above for a monopolistically competitive firm in short-run equilibrium. This firm will realize an economic A. profit of $480. B. profit of $600. C. profit of $280. D. loss of $320.

C) a monopolistically competitive industry. D) an oligopolistic industry. E) None of the above - it is not a long-run equilibrium. 33) Refer to Figure 11-2. The position of a typical firm when the industry is in long -run equilibrium with free entry and exit and product differentiation is exhibited in diagram A) A. B) B. C) C. D) D. 34) In long ...

Refer to the diagram for a monopolistically competitive firm. long-run equilibrium price will be.

Figure 13 - 14 illustrates a monopolistically competitive firm. 7) Refer to Figure 13 -14. Which of the following statements describes the firm depicted in the diagram? 7) A) The firm is making no economic profit and will exit the industry. B) The firm is in long - run equilibrium and is breaking even.

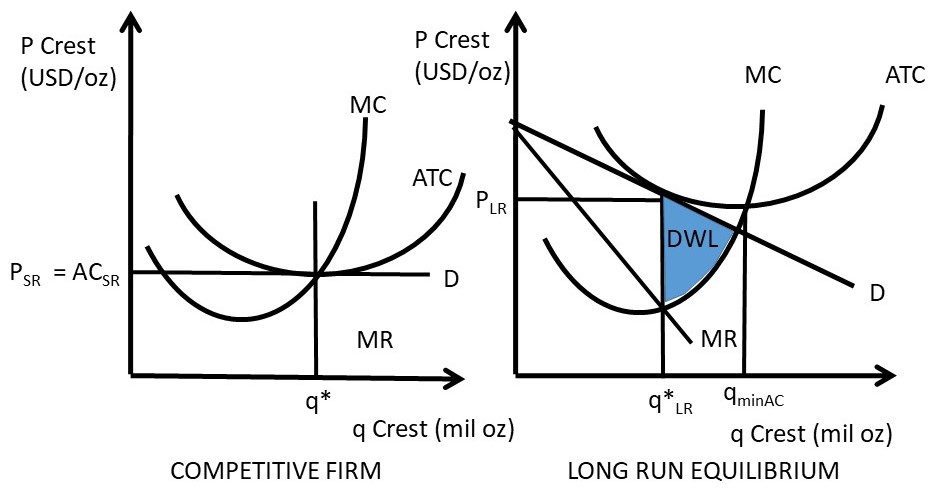

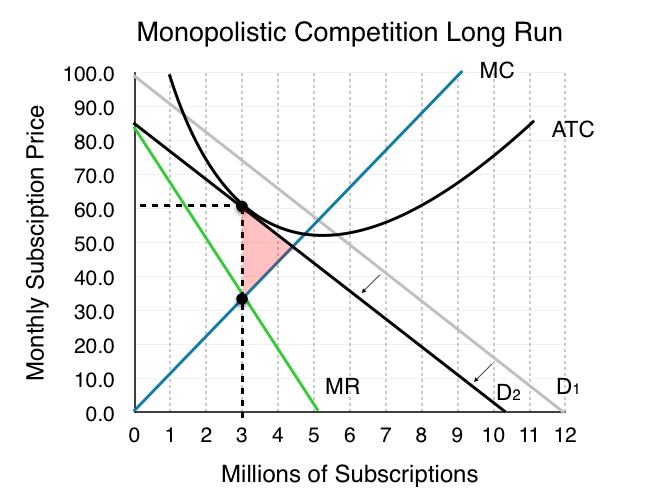

When a monopolistically competitive firm is in long-run equilibrium, MR = MC and P > minimum ATC. Refer to the diagram. The monopolistically competitive firm shown is realizing an economic profit. In the long run, the price charged by the monopolistically competitive firm attempting to maximize profits will be equal to ATC.

Refer to the above graphs. The long-run equilibrium for a monopolistically competitive firm is represented by graph -B. 52. Refer to the diagram for a monopolistically competitive firm. If more firms were to enter the industry and product differentiation were to weaken, then -the demand curve would become more elastic. 53. Refer to the diagrams.

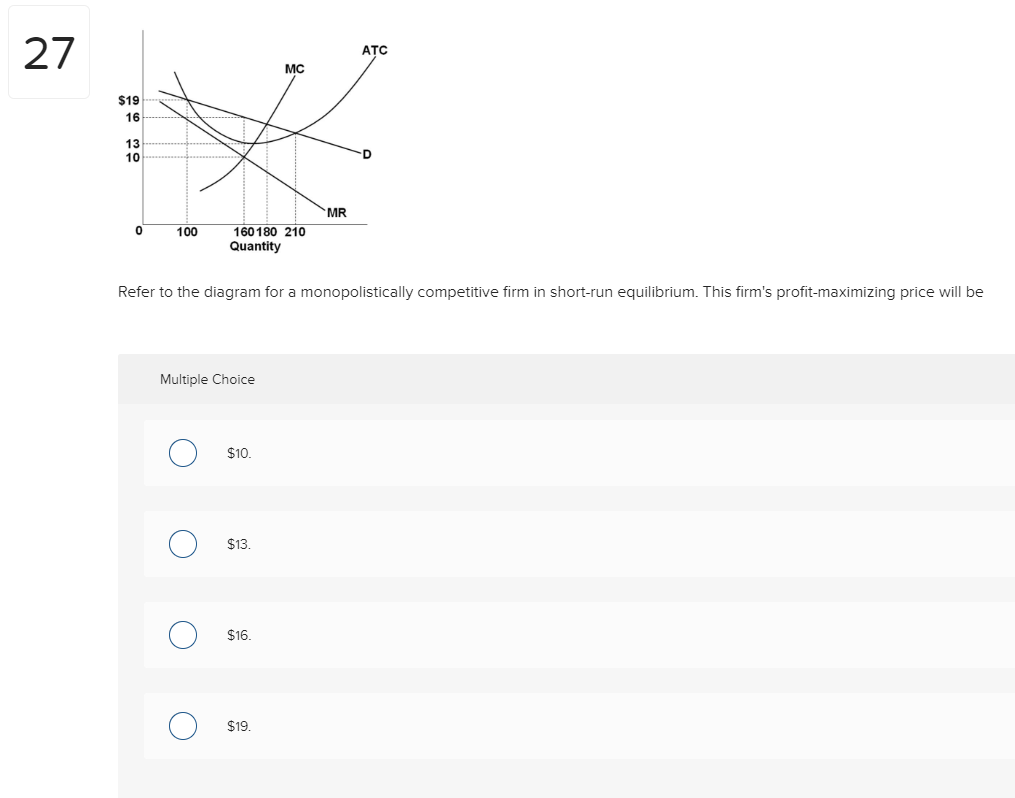

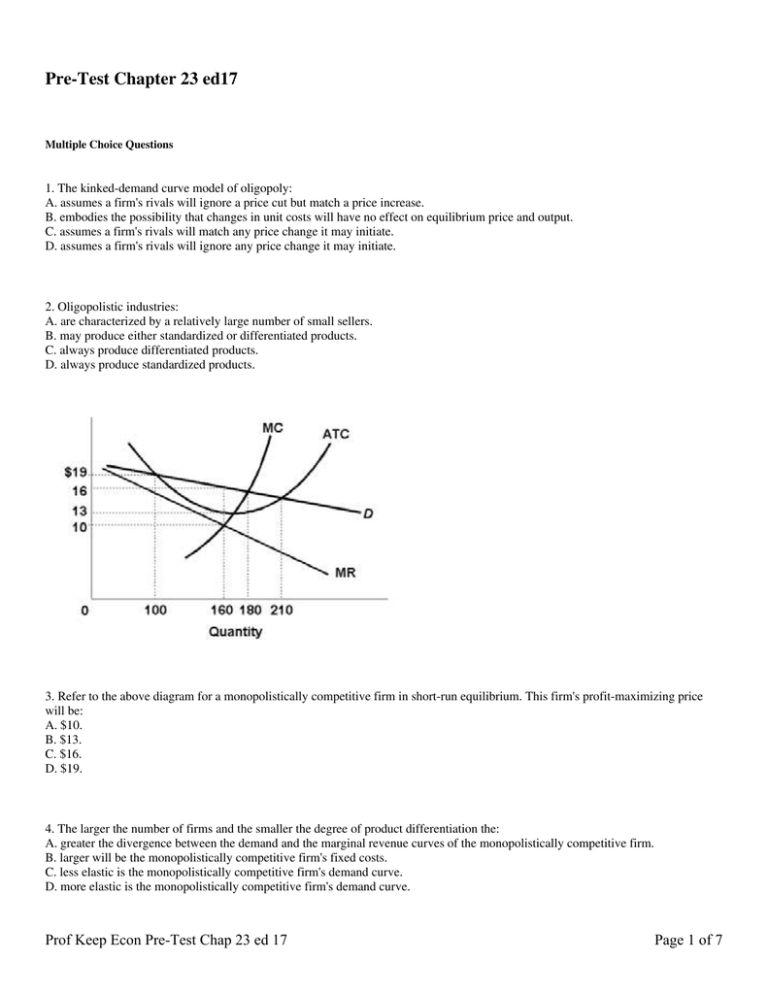

Refer to the above diagram for a monopolistically competitive firm in short-run equilibrium. This firm's profit-maximizing price will be: A. $10. B. $13. C. $16. D. $19. 5. R-1 F25030 ... In long-run equilibrium a monopolistically competitive firm will: A. earn an economic profit. ...

Economics questions and answers. 1.Refer to the above diagram for a monopolistically competitive firm. Long-run equilibrium output will be: a. greater than E. b. E. c. D. d. C. 2.Refer to the diagram. In short-run equilibrium, the monopolistically competitive firm shown.

(6) Under perfect competition the firm in the long run makes only normal profits but under monopoly the firm can get super-normal profits even in the long run. (7) Since, even in the long run, the monopolist's demand curve remains downward sloping, it cannot be tangent to average cost curve at AC min .

• Economic profits driven to zero in long run Monopolistic Competition Red=4 largest. Green=5-8 Blue=9-20 The numbers are the HHI. Market Share in Monopolistic Competition Output and Price in Monopolistic Competition The Firm's Short-Run Output and Price Decision Holding quality and marketing constant, profit

3. Refer to the above diagram for a monopolistically competitive firm in short-run equilibrium. This firm will realize an economic: A. loss of $320. B. profit of $480. C. profit of $280. D. profit of $600.

Purely competitive firms monopolistically competitive firms and pure monopolies all earn zero economic profits in the long run. 1refer to the above diagram for a monopolistically competitive firm. Let us learn about the short run and long run equilibrium of a firm under monopolistic competition. 4both diagrams b and c. 3refer to the diagram above.

A) The firm's... 1) In both monopolistically competitive and perfectly competitive industries A) firms produce products for which there are no close substitutes. B) there are high barrier... 11) Economists have long debated whether there is a significant loss of well-being to society in markets that are monopolistically competitive rather than ...

33) In the long run, monopolistically competitive firms produce where . A) excess capacity exists . B) the markup is equal to zero . C) the demand curve has shifted so that it intersects the minimum average total cost point . D) average total cost is minimized . Answer: A . 34) In monopolistic competition, in the long run firms produce

A) equilibrium output would rise and equilibrium price would fall. B) the demand curve would become more elastic. C) equilibrium output would decline and equilibrium price would rise. D) none of these above. B. Refer to the diagram below for a monopolistically competitive firm in short-run equilibrium.

Pre-test chapter 23 chapter 23 ed17.pdf‚ &sbquo ...

160. Refer to the above diagram for a monopolistically competitive firm in short-run equilibrium. This firm will realize an economic: profit of $480. Refer to the above diagrams, which pertain to monopolistically competitive firms. Short-run equilibrium entailing economic loss is shown by: diagram c only.

Micro chart questions flashcards | quizlet

Therefore, at the long-run equilibrium output at the MR = LMC point, we have, for the monopolist, p > LMC. In other words, in the long-run equilibrium, price is equal to marginal cost for the competitive firm and price is greater than marginal cost for the monopolistic firm.

5.2: monopolistic competition - social sci libretexts

40)In the long run, a firm in a monopolistically competitive industry produces where its marginal cost A)equals its price. B)is less than its average cost. C)equals its average cost. D)exceeds its average cost. 40) 41)In the long run, a firm in monopolistic competition produces where the slope of the average total cost curve is A)zero.

Econ 212-micro chapter 13 quiz flashcards | quizlet

The monopolistically competitive firm's long‐run equilibrium situation is illustrated in Figure .. The entry of new firms leads to an increase in the supply of differentiated products, which causes the firm's market demand curve to shift to the left. As entry into the market increases, the firm's demand curve will continue shifting to the left until it is just tangent to the average total ...

Mc atc mc atc -d mr mr 0 0 (b) mc atc d mr (c) 65.... - itprospt

Eventually, the monopolistically competitive firm will reach long-run equilibrium (profit-maximization) position whereby it receives a price (P) that is equal to the Long-run Average Total Cost (LAC) so that it will be earning only a normal profit as illustrated in Figure 10.6. Fig. 10.6: Long-run profit-maximising position of a ...

Long-run equilibrium under each market structure ...

The long-run equilibrium position of the monopolistically competitive firm occurs at a point where average costs are - constant. - increasing. - decreasing. - at their minimum point. decreasing Refer to the diagram. The monopolistically competitive firm shown - will realize allocative efficiency at its profit-maximizing output.

Tutorial 9 solutions - tutorial – solutions chapter 16 ...

7. Economic analysis of a monopolistically competitive industry is more complicated than that of pure competition because: A) the number of firms in a monopolistic competitive industry is larger. B) monopolistically competitive firms realize economic profits in the long run. C) of product differentiation and consequent advertising activities.

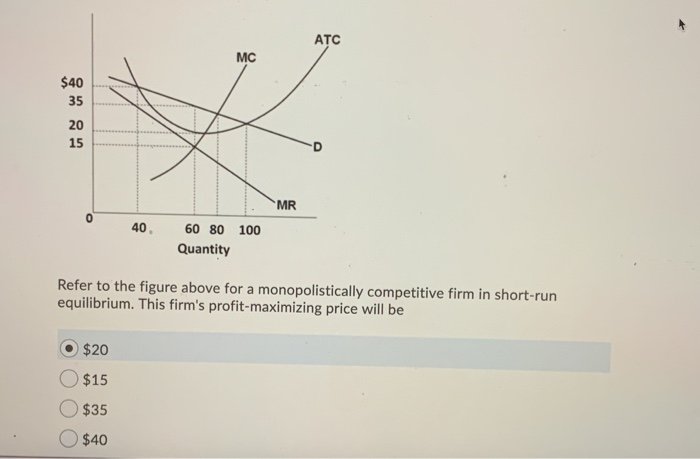

Solved mr 40. 60 80 100 quantity refer to the figure above ...

In the long run, economic theory predicts that a monopolistically competitive firm will have excess production capacity. Refer to the diagram for a monopolistically competitive firm in short-run equilibrium.

Use the table below to answer the following two questions

2. the equilibrium position of a competitive firm in the long run. 3. a competitive firm that is realizing an economic profit. 4. the loss-minimizing position of a competitive firm in the short run. 9. Refer to the above diagram. If this competitive firm produces output Q, it will: 1. suffer an economic loss. 2. earn a normal profit.

8.4 monopolistic competition – principles of microeconomics

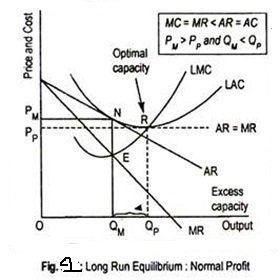

Long run equilibrium is achieved at point E where LMC equals MR (Fig. 5.16). The equilibrium output thus determined is OQ M. At this output, AR equals AC. The firm gets normal profit by selling OQ M output at the price OP M. Note that a monopolistically competitive firm always operates somewhere to the left of the minimum point of its AC curve.

Chapter 13 (monopolistic competition) homework flashcards ...

Equilibrium under Monopolistic Competition. The two types of demand curves of a firm under monopolistic competition are due to the following reasons:. When a firm revises the price of its product, the rival firms don't always increase the prices of their products too.Therefore, the demand curve has a smaller slope and the demand for the product is more elastic.

8.4 monopolistic competition – principles of microeconomics

Chapter 9: four market models

Practice free response questions - ppt video online download

11a problem

File:long-run equilibrium of the firm under monopolistic ...

Revmncmp

Econ 150 ch 13 monopolistic competition & oligopolies ...

Pre-test chapter 23 chapter 23 ed17.pdf‚ &sbquo ...

✓ solved: draw and explain a diagram to show the long-run ...

Solved refer to the diagram for a monopolistically | chegg.com

Equilibrium of a firm under monopolistic competition ...

Monopolistic competition - wikipedia

Long run equilibrium of competitive firm and industry

Econ 212-micro chapter 13 quiz flashcards | quizlet

Solved 27 atc mc $19 16 13 10 mr 0 100 160180 210 quantity ...

Solved ic6 monopolistic competition 0 100 160 180 210 | chegg.com

Unit 3 practice test

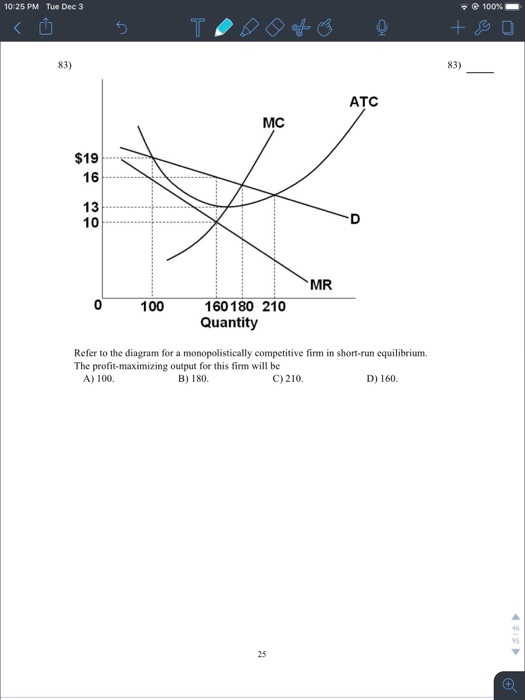

Solved 100% 10:25 pm tue dec 3 t 83) 83) аtс mc $19 16 13 10 ...

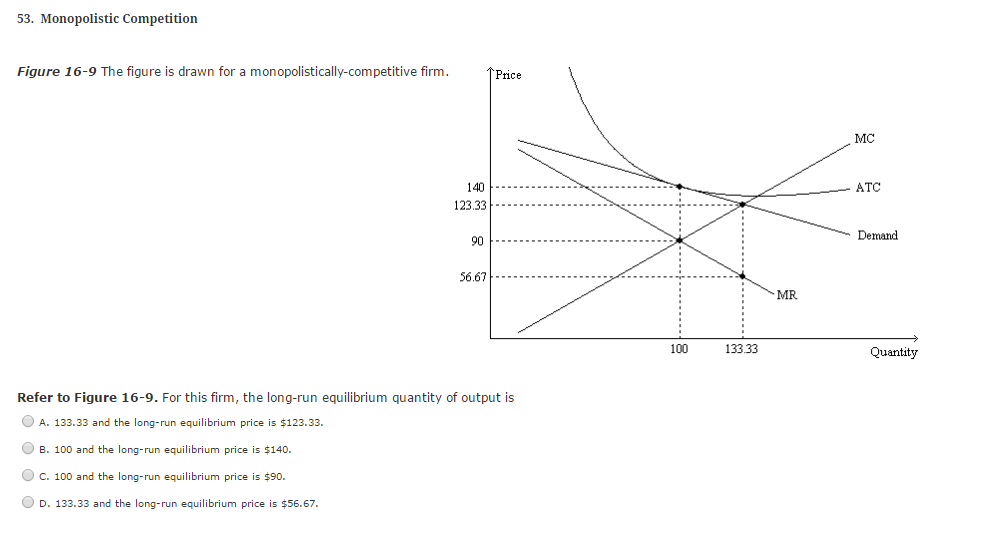

Solved 53. monopolistic competition figure 16-9 the figure ...

Solved $ mc atc a demand mr de quantity refer to the diagram ...

Graph the long-run profit of a monopolistically competitive ...

8.4 monopolistic competition – principles of microeconomics

Pre-test chapter 23 ed17 - pdf free download

Solved) - the graph below shows a monopolistically ...

Pre-test chapter 23 ed17

Solved refer to the diagram above for a monopolistically ...

Long-run economic profit for perfectly competitive firms

Econ 212-micro chapter 13 quiz flashcards | quizlet

Entry, exit and profits in the long run | microeconomics

0 Response to "41 refer to the diagram for a monopolistically competitive firm. long-run equilibrium price will be"

Post a Comment